Navigating the Medicare Maze UnitedHealthcare Supplement Plans through AARP

Medicare. It’s a word that echoes with both promise and perplexity. As you approach retirement, navigating the labyrinthine landscape of healthcare options can feel overwhelming. This is where Medicare Supplement insurance, sometimes offered through organizations like AARP, enters the equation. Specifically, plans provided by UnitedHealthcare (UHC) through AARP represent a significant segment of this market.

UnitedHealthcare’s presence in the Medicare Supplement arena combined with AARP's extensive membership network offers a compelling proposition for many. But what exactly does a UHC Medicare Supplement Plan procured through AARP entail? These plans, also known as Medigap, are designed to fill the gaps in Original Medicare coverage, potentially alleviating the financial burden of copayments, coinsurance, and deductibles. This article delves into the intricacies of these plans, providing you with the knowledge necessary to make informed decisions about your healthcare future.

Understanding the history and context of Medigap is crucial. Original Medicare, established in 1965, doesn't cover all healthcare expenses. This realization led to the creation of Medicare Supplement insurance to help mitigate out-of-pocket costs. AARP's role in advocating for seniors and providing access to insurance options has positioned it as a key player in this space. UHC's collaboration with AARP offers a platform for seniors to access a range of Medigap plans, leveraging the strengths of both organizations.

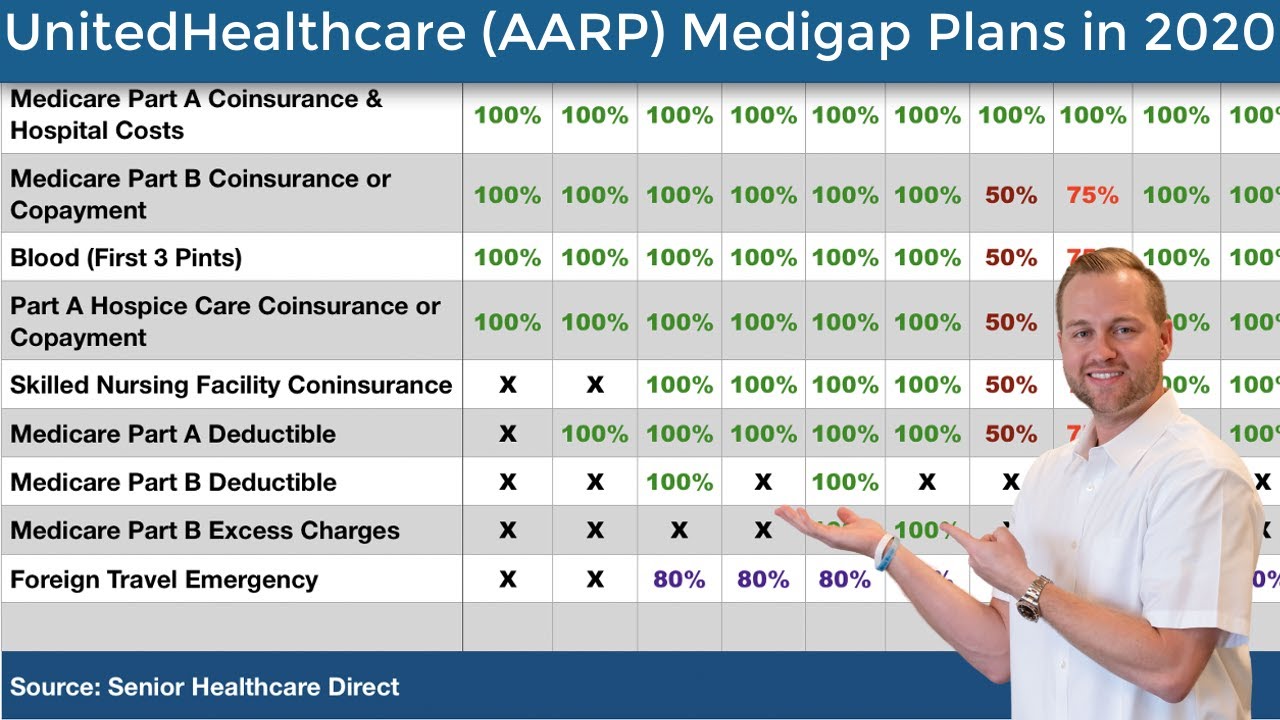

One of the central issues surrounding UHC Medicare Supplement plans, and Medigap policies in general, is choosing the right plan. The standardized plan letters (A, B, C, D, F, G, K, L, M, and N) can be confusing. Each plan offers different levels of coverage, and selecting the appropriate one depends on your individual health needs, budget, and risk tolerance. Understanding these nuances is critical to maximizing your benefits and minimizing your financial exposure.

For instance, Plan G offered by UHC through AARP generally covers most out-of-pocket expenses, with the exception of the Part B deductible. Plan N, another popular option, covers most costs but leaves you responsible for some copays and excess charges. Understanding these differences, along with the premium costs associated with each plan, is fundamental to making an informed choice. Consulting with a licensed insurance agent specializing in Medicare can provide personalized guidance.

Three key benefits of UHC Medicare Supplement plans obtained through AARP often include network flexibility, predictable costs, and foreign travel emergency coverage. Network flexibility means you can generally see any doctor who accepts Medicare, eliminating the restrictions of narrow networks. Predictable costs, through coverage of copays and coinsurance, help you budget your healthcare expenses. And foreign travel emergency coverage provides peace of mind for those who travel abroad.

Advantages and Disadvantages of UHC Medicare Supplement Plans through AARP

| Advantages | Disadvantages |

|---|---|

| Access to UHC's network | Premium costs can be substantial |

| AARP member benefits | Doesn't cover everything (e.g., vision, dental, hearing) |

| Standardized plans for easy comparison | May not be the most cost-effective option for everyone |

Frequently Asked Questions:

1. What is the difference between Medicare Advantage and Medicare Supplement?

(Medicare Advantage is an alternative to Original Medicare, while a Supplement complements it.)

2. How do I enroll in a UHC Medicare Supplement plan through AARP?

(Contact a licensed insurance agent or visit the UHC/AARP websites.)

3. When can I enroll in a Medigap plan?

(Your Medigap Open Enrollment Period is the best time.)

4. Are there any age restrictions for UHC Medicare Supplement plans?

(Generally available to those eligible for Medicare.)

5. Can I change my UHC Medicare Supplement plan later?

(Yes, but it might require undergoing medical underwriting.)

6. What factors influence the cost of premiums?

(Age, location, plan chosen, tobacco use.)

7. Does a UHC Medigap plan cover prescription drugs?

(No, you need a separate Part D plan.)

8. Can I use my UHC Medicare Supplement plan with any doctor?

(Generally, any doctor who accepts Medicare.)

In conclusion, securing reliable healthcare coverage in retirement is paramount. UHC Medicare Supplement plans available through AARP provide a pathway to navigate the complexities of Medicare, offering a range of options to address various needs and budgets. While navigating the choices can be challenging, understanding the nuances of Medigap, plan benefits, and the role of organizations like AARP and UHC empowers you to make informed decisions, securing your healthcare future and providing peace of mind. Take the time to research, compare plans, consult with professionals, and choose the coverage that best aligns with your individual circumstances. Your health and financial well-being deserve nothing less.

Capricorn and taurus match a celestial love story

Decoding benjamin moore rose hues

Transform your space with the serene hues of sherwin williams soft blue

.jpeg)

{kind=link}